India’s Fintech Revolution: A Strategic Lifeline for SMEs

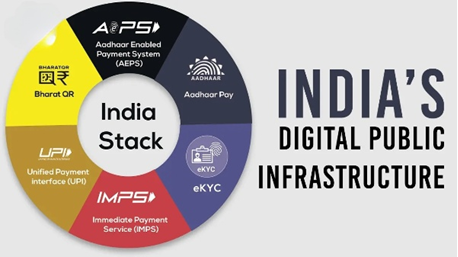

India’s financial services sector is in the midst of a structural transformation, driven by a unique interplay of technology, policy, and entrepreneurship. The Aadhaar identity system, the Unified Payments Interface (UPI), and the institutional support of the National Payments Corporation of India (NPCI) have together created one of the world’s most inclusive digital infrastructures. This digital public stack has not only brought millions into the formal economy but also lowered the cost of financial inclusion and opened fertile ground for fintech innovation at scale.

The impact is staggering. By 2030, India’s fintech market is projected to reach $550 billion, growing at a compound annual rate of over 30%. Adoption stands at 87%, the highest globally, underscoring how deeply embedded fintech has become in daily economic life. Yet behind these figures lies the real story: how fintech is reshaping opportunities for India’s small and medium enterprises (SMEs), which form the backbone of the economy.

SMEs at the Centre

India is home to more than 63 million MSMEs, which collectively contribute nearly 30% of GDP and employ over 110 million people. Despite their centrality, these enterprises have long faced structural barriers, limited access to formal finance, cumbersome compliance processes, and outdated workflows. Traditional banks often viewed SMEs as high-risk, with insufficient collateral and thin credit histories.

Fintechs are rewriting this narrative. By leveraging Aadhaar-based eKYC, UPI’s real-time payments infrastructure, GST data, and the emerging Account Aggregator framework, fintech firms are providing SMEs with digital-first solutions: collateral-free working capital loans, automated compliance systems, digitized bookkeeping, payroll integration and supply-chain financing. These innovations are lowering costs, improving transparency and enabling SMEs to scale operations more rapidly.

The story of Tide, a UK-based fintech that recently achieved unicorn status while expanding aggressively in India, illustrates the global recognition of India’s SME opportunity. Tide’s digital-first banking model is tailor-made for small businesses. At the same time, India’s homegrown fintechs are building equally impactful solutions designed for the unique needs of local enterprises.

Indian Fintechs Powering Small Businesses

Several fintechs have emerged as key enablers for SME growth. Khatabook and OkCredit started as digital ledger platforms but have since evolved into comprehensive financial tools that digitize credit records and cash flows for millions of small merchants. Razorpay, best known for its payment gateway, has expanded into SME banking through RazorpayX, offering payroll automation, vendor payments and working capital solutions.

On the lending side, firms like Indifi Technologies, Capital Float and FlexiLoans are addressing the credit gap by using alternative data from e-commerce transactions to GST filings to assess creditworthiness. This allows SMEs to access loans without the collateral traditionally demanded by banks. Meanwhile, CredAble and TartanHQ are innovating in payroll-linked advances and supply-chain financing, easing liquidity bottlenecks.

Other platforms such as Mswipe, Finova Capital, and Infibeam Avenues are extending digital payments and merchant services deeper into semi-urban and rural markets. Even niche players like Refyne, with its salary-on-demand model, and Rupeek, with its digital gold loans, are expanding financial options for smaller businesses and their employees. Collectively, these fintechs are reducing the friction that has historically stifled SME competitiveness.

Streamlining Compliance and Workflows

For SMEs, compliance is often as burdensome as access to capital. Frequent regulatory updates, complex tax filings and labor law requirements can drain resources and management focus. Fintechs are easing this burden by integrating compliance tools into day-to-day operations. Automated GST reconciliation, invoice matching and digital tax filing platforms are helping SMEs maintain transparency while reducing costs.

This compliance innovation extends to global opportunities. As international buyers increasingly demand rigorous ESG standards and documentation, fintech-enabled platforms are helping SMEs meet audit and traceability requirements. By doing so, they enhance the credibility of Indian SMEs in global supply chains and open doors to export markets.

Policy and Infrastructure Enablers

The success of fintech in SME empowerment is inseparable from India’s policy and infrastructure framework. The JAM trinity- Jan Dhan, Aadhaar and Mobile brought millions into the banking system and drastically reduced onboarding costs. UPI revolutionized payments, while NPCI products such as AePS (Aadhaar-enabled Payment System) extended banking to the remotest corners of the country.

More recently, the Account Aggregator framework is facilitating secure data sharing between banks, fintechs and borrowers, enabling faster, more accurate credit decisions. Government programs like Digital MSME, the Open Credit Enablement Network (OCEN) and PLI schemes are further promoting formalization and digitization, expanding the fintech addressable market. Infrastructure projects like Dedicated Freight Corridors and digital documentation at ports complement this ecosystem by lowering transaction costs for SMEs engaged in trade.

Challenges That Remain

While the progress is remarkable, challenges persist. Data privacy and cybersecurity risks loom large as SMEs digitize their financial operations. Regulatory uncertainty can create hesitation for both fintechs and their SME clients. Smaller fintechs also struggle with scaling sustainably, while digital literacy gaps in rural areas limit the reach of otherwise transformative solutions.

There is also the danger of over-indebtedness if access to easy credit outpaces financial literacy. Policymakers and regulators must therefore balance innovation with safeguards, fostering trust while allowing space for experimentation through regulatory sandboxes and harmonized standards.

Outlook

India’s fintech ecosystem is no longer a niche sector it is the lifeline powering the next phase of SME growth. From a Kirana shop digitizing daily accounts to a mid-sized manufacturer securing ESG-linked supply-chain finance, the spectrum of fintech-enabled transformation is expanding rapidly.

With projections of a $550 billion market size by 2030, the coming decade will be defined by how well fintechs integrate into SME workflows, scale responsibly and build trust. For banks and investors, the SME fintech space represents not only commercial opportunity but also a strategic lever for inclusive economic growth.

In many ways, India’s fintech revolution is a blueprint for the world: how digital public goods, when combined with entrepreneurial innovation, can unlock broad-based prosperity. By continuing to align compliance, competitiveness and innovation, India is not just digitizing small businesses it is fundamentally rewriting the rules of financial inclusion for the 21st century.